forum

library

tutorial

contact

Solar Panels Could Destroy U.S. Utilities,

According to U.S. Utilities

by David Roberts

Grist Magazine, May 2013

|

the film forum library tutorial contact |

|

Solar Panels Could Destroy U.S. Utilities,

by David Roberts

|

Solar power and other distributed renewable energy technologies could lay waste to U.S. power utilities and burn the utility business model, which has remained virtually unchanged for a century, to the ground.

Solar power and other distributed renewable energy technologies could lay waste to U.S. power utilities and burn the utility business model, which has remained virtually unchanged for a century, to the ground.

That is not wild-eyed hippie talk. It is the assessment of the utilities themselves.

Back in January, the Edison Electric Institute -- the (typically stodgy and backward-looking) trade group of U.S. investor-owned utilities -- released a report [PDF] that, as far as I can tell, went almost entirely without notice in the press. That's a shame. It is one of the most prescient and brutally frank things I've ever read about the power sector. It is a rare thing to hear an industry tell the tale of its own incipient obsolescence.

I've been thinking about how to convey to you, normal people with healthy social lives and no time to ponder the byzantine nature of the power industry, just what a big deal the coming changes are. They are nothing short of revolutionary . . . but rather difficult to explain without jargon.

So, just a bit of background. You probably know that electricity is provided by utilities. Some utilities both generate electricity at power plants and provide it to customers over power lines. They are "regulated monopolies," which means they have sole responsibility for providing power in their service areas. Some utilities have gone through deregulation; in that case, power generation is split off into its own business, while the utility's job is to purchase power on competitive markets and provide it to customers over the grid it manages.

This complexity makes it difficult to generalize about utilities . . . or to discuss them without putting people to sleep. But the main thing to know is that the utility business model relies on selling power. That's how they make their money. Here's how it works: A utility makes a case to a public utility commission (PUC), saying "we will need to satisfy this level of demand from consumers, which means we'll need to generate (or purchase) this much power, which means we'll need to charge these rates." If the PUC finds the case persuasive, it approves the rates and guarantees the utility a reasonable return on its investments in power and grid upkeep.

Thrilling, I know. The thing to remember is that it is in a utility's financial interest to generate (or buy) and deliver as much power as possible. The higher the demand, the higher the investments, the higher the utility shareholder profits. In short, all things being equal, utilities want to sell more power. (All things are occasionally not equal, but we'll leave those complications aside for now.)

Now, into this cozy business model enters cheap distributed solar PV, which eats away at it like acid.

First, the power generated by solar panels on residential or commercial roofs is not utility-owned or utility-purchased. From the utility's point of view, every kilowatt-hour of rooftop solar looks like a kilowatt-hour of reduced demand for the utility's product. Not something any business enjoys. (This is the same reason utilities are instinctively hostile to energy efficiency and demand response programs, and why they must be compelled by regulations or subsidies to create them. Utilities don't like reduced demand!)

It's worse than that, though. Solar power peaks at midday, which means it is strongest close to the point of highest electricity use -- "peak load." Problem is, providing power to meet peak load is where utilities make a huge chunk of their money. Peak power is the most expensive power. So when solar panels provide peak power, they aren't just reducing demand, they're reducing demand for the utilities' most valuable product.

But wait. Renewables are limited by the fact they are intermittent, right? "The sun doesn't always shine," etc. Customers will still have to rely on grid power for the most part. Right?

This is a widely held article of faith, but EEI (of all places!) puts it to rest. (In this and all quotes that follow, "DER" means distributed energy resources, which for the most part means solar PV.)

Due to the variable nature of renewable DER, there is a perception that customers will always need to remain on the grid. While we would expect customers to remain on the grid until a fully viable and economic distributed non-variable resource is available, one can imagine a day when battery storage technology or micro turbines could allow customers to be electric grid independent. To put this into perspective, who would have believed 10 years ago that traditional wire line telephone customers could economically "cut the cord?" [Emphasis mine.]Indeed! Just the other day, Duke Energy CEO Jim Rogers said, "If the cost of solar panels keeps coming down, installation costs come down and if they combine solar with battery technology and a power management system, then we have someone just using [the grid] for backup." What happens if a whole bunch of customers start generating their own power and using the grid merely as backup? The EEI report warns of "irreparable damages to revenues and growth prospects" of utilities.

Utility investors are accustomed to large, long-term, reliable investments with a 30-year cost recovery -- fossil fuel plants, basically. The cost of those investments, along with investments in grid maintenance and reliability, are spread by utilities across all ratepayers in a service area. What happens if a bunch of those ratepayers start reducing their demand or opting out of the grid entirely? Well, the same investments must now be spread over a smaller group of ratepayers. In other words: higher rates for those who haven't switched to solar.

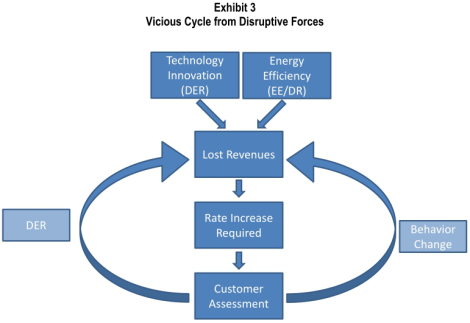

That's how it starts. These two paragraphs from the EEI report are a remarkable description of the path to obsolescence faced by the industry:

The financial implications of these threats are fairly evident. Start with the increased cost of supporting a network capable of managing and integrating distributed generation sources. Next, under most rate structures, add the decline in revenues attributed to revenues lost from sales foregone. These forces lead to increased revenues required from remaining customers . . . and sought through rate increases. The result of higher electricity prices and competitive threats will encourage a higher rate of DER additions, or will promote greater use of efficiency or demand-side solutions.Did you follow that? As ratepayers opt for solar panels (and other distributed energy resources like micro-turbines, batteries, smart appliances, etc.), it raises costs on other ratepayers and hurts the utility's credit rating. As rates rise on other ratepayers, the attractiveness of solar increases, so more opt for it. Thus costs on remaining ratepayers are even further increased, the utility's credit even further damaged. It's a vicious, self-reinforcing cycle:Increased uncertainty and risk will not be welcomed by investors, who will seek a higher return on investment and force defensive-minded investors to reduce exposure to the sector. These competitive and financial risks would likely erode credit quality. The decline in credit quality will lead to a higher cost of capital, putting further pressure on customer rates. Ultimately, capital availability will be reduced, and this will affect future investment plans. The cycle of decline has been previously witnessed in technology-disrupted sectors (such as telecommunications) and other deregulated industries (airlines).

One implication of all this -- a poorly understood implication -- is that rooftop solar fucks up the utility model even at relatively low penetrations, because it goes straight at utilities' main profit centers. (It's already happening in Germany.) Right now, distributed solar PV is a relatively tiny slice of U.S. electricity, less than 1 percent. For that reason, utility investors aren't paying much attention. "Despite the risks that a rapidly growing level of DER penetration and other disruptive challenges may impose," EEI writes, "they are not currently being discussed by the investment community and factored into the valuation calculus reflected in the capital markets." But that 1 percent is concentrated in a small handful of utility districts, so trouble, at least for that first set of utilities, is just over the horizon. Utility investors are sleepwalking into a maelstrom.

("Despite all the talk about investors assessing the future in their investment evaluations," the report notes dryly, "it is often not until revenue declines are reported that investors realize that the viability of the business is in question." In other words, investors aren't that smart and rational financial markets are a myth.)

Bloomberg Energy Finance forecasts 22 percent compound annual growth in all solar PV, which means that by 2020 distributed solar (which will account for about 15 percent of total PV) could reach up to 10 percent of load in certain areas. If that happens, well:

Assuming a decline in load, and possibly customers served, of 10 percent due to DER with full subsidization of DER participants, the average impact on base electricity prices for non-DER participants will be a 20 percent or more increase in rates, and the ongoing rate of growth in electricity prices will double for non-DER participants (before accounting for the impact of the increased cost of serving distributed resources).So rates would rise by 20 percent for those without solar panels. Can you imagine the political shitstorm that would create? (There are reasons to think EEI is exaggerating this effect, but we'll get into that in the next post.)

If nothing is done to check these trends, the U.S. electric utility as we know it could be utterly upended. The report compares utilities' possible future to the experience of the airlines during deregulation or to the big monopoly phone companies when faced with upstart cellular technologies. In case the point wasn't made, the report also analogizes utilities to the U.S. Postal Service, Kodak, and RIM, the maker of Blackberry devices. These are not meant to be flattering comparisons.

Remember, too, that these utilities are not Google or Facebook. They are not accustomed to a state of constant market turmoil and reinvention. This is a venerable old boys network, working very comfortably within a business model that has been around, virtually unchanged, for a century. A friggin' century, more or less without innovation, and now they're supposed to scramble and be all hip and new-age? Unlikely.

So what's to be done? You won't be surprised to hear that EEI's prescription is mainly focused on preserving utilities and their familiar business model. But is that the best thing for electricity consumers? Is that the best thing for the climate?

We'll dig into those questions in my next post.

learn more on topics covered in the film

see the video

read the script

learn the songs

discussion forum